A 9-Year-Old Saved $24 In 11 Weeks: How To Teach Kids About Money

When Camila’s best friend got a phone and Mari said “not right now,” her nine-year-old answered flatly: “We never can.” That quiet resignation is what sent Mari looking for how to teach a child about money – not a lecture, but a way to change what Camila believed about it.

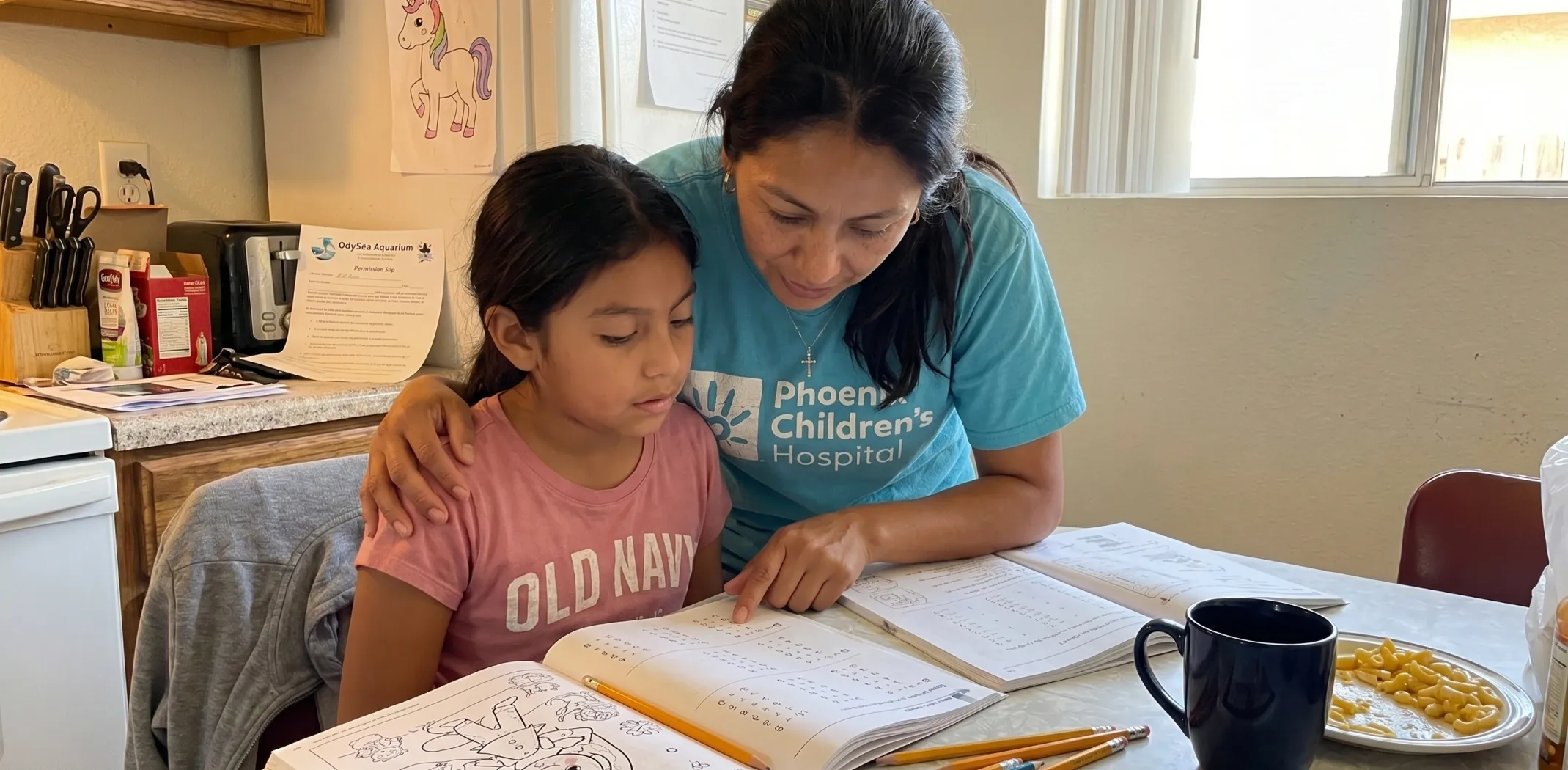

Mari is 34, a teacher’s aide at a Title-I school in Phoenix, raising Camila on $32,400 a year. There was $214 in checking on the 28th and a credit-card balance that had not moved in two years. She was not failing her daughter – she just had no words, and no plan, for the questions Camila kept asking.

What changed it was not more money. It was a short setup that became a weekly routine – three little jars, one calm money chat, and the exact words for the questions that used to make Mari freeze. Here is the order she did it in.

Why “we cannot afford it” quietly teaches the wrong lesson

“We cannot afford it” ends the conversation, but it teaches a child that money is a wall, not a tool. What a kid hears is “we are stuck,” not “here is how choices work.” The gap was never Mari’s love or effort – it was that no one had given her the words to turn a hard moment into a lesson.

The hopeful part: a small income is not a barrier to teaching this – in some ways it is the perfect classroom. A few dollars, three jars and the right words turn “we never can” into “here is how we choose.” That is exactly what a guided plan hands a stretched parent.

Mari was not raising an entitled kid, and she was not doing anything wrong. She simply had no framework – no jars, no script – for turning a painful “we never can” into a lesson Camila could use.

Like a lot of parents on a tight budget, Mari did not need a guilt trip about money. She needed the words for the questions that ambushed her – and a way to make the answer real.

What Mari tried first – and why none of it stuck

Before the plan that worked, she tried the usual things:

Just saying “we cannot afford it”

True, but it landed as a door closing. Camila heard a limit on the family, not a lesson she could do anything with – and it quietly taught helplessness.

Overexplaining the whole budget

Dumping rent, the car and the card on a nine-year-old only made Camila anxious. A child needs one clear idea, not the adult weight of it all.

Hoping the school would cover it

It never really does. Money is learned at home first – and without a plan, “they will teach it eventually” meant no one did.

Every response was either a shutdown or too much at once. None did the thing that teaches a kid: one small idea a week, made physical with jars, plus a calm script for the questions that hurt.

I did not need more money to teach her about money. I needed the right sentence for “we never can” – and three jars to show her that we could choose.

The 4 things the Course built for Mari and Camila

She answered a few quick questions – Camila’s age, the “we never can” moment, and the time they had. Minutes later she had four things, built for a busy single parent:

It did not hand me a budget to explain. It gave me one sentence for the question I dreaded, and three jars – and Camila stopped hearing “no” and started hearing “choose.”

Week one was small: set up the jars and split a few dollars. No speech about the budget. Camila chose the amounts, and for the first time money felt like something she got to steer, not something that only happened to them.

From “we never can” to paying for her own field trip: 11 weeks

The plan ran fifteen minutes a week – one idea, the jars, one question. Small week after small week, Camila’s whole tone about money shifted.

🫙 SAVE ★ the jar that changed the story

A goal she chose herself – her school field trip – and eleven weeks of coins that proved “we never can” was not true.

💵 SPEND

Hers to enjoy – a small, visible amount that made “want it now” a choice she could weigh, not a fight.

🎁 SHARE

A little for someone else – the jar that showed even a tight budget has room to give.

By week eleven, the moment came: Camila handed Mari $24 in coins and asked to pay for her own school field trip. Not because money was suddenly easy – but because she finally believed she had a say in it.

The $24 was not the point. It was Camila going from “we never can” to “I saved for this myself.” That is what the weeks really bought – not a jar of coins, but a nine-year-old who believes she has choices.

Why “kids on a budget cannot learn about money” is a myth

There is a belief that money lessons are for families with money to spare. The opposite is true – a tight budget is where choices are most real, so the lessons land hardest. A child with a few dollars and three jars learns trade-offs a wealthy kid never has to face. Scarcity handled well is not a disadvantage; with the right words, it is the best money classroom there is.

An app or a book can help, but neither gives a stretched parent a weekly plan, the jars, and the exact sentence for the question that stings – matched to the child in front of you. That gap is the whole point.

We are on a really tight budget – is this even for us?

Especially for you. The lessons run on a few coins, not a big allowance, and a tight budget makes the choices more real, not less. Mari taught Camila on $32,400 a year – the jars and the scripts do not need money to spare, just a few minutes a week.

What other parents did with the same plan

Mari’s story is common: caring parents, big questions from small kids, and no ready words – until the plan gave them a routine and a script.

“My twins are 7 and fight about money. The plan came back with two versions, because they have different personalities. I cried. Twin one stopped asking for stuff in the Target checkout line by week five.”

Jessica P. · mom of twins

“My son asked why our family does not have what his cousin’s has. I used to freeze on that one. The script gave me the actual sentence. It worked the first time I used it.”

Monica R. · single mom of one, El Paso TX

Beyond the weekly plan, Kids Financial Literacy Course includes printable jar labels, a bank of scripts for the tough questions, and age bands so the same plan grows with your child – from first coins to a first debit card.

Different kids, different questions, the same first move: stop reaching for “we cannot afford it,” set a weekly time, and make money a choice a child can see.

How to teach a child about money: the 5-step playbook

If the hard questions keep catching you flat, here is the order that changes it – the same one the Course walks you through:

Swap “we cannot” for “we choose”

The single most important shift: money is a set of choices, not a wall. It changes what a child believes is possible.

Make it physical with three jars

SAVE, SPEND, SHARE. A few real coins a child splits by hand teaches more than any budget conversation.

Keep a script for the hard question

Have the calm sentence ready for “why can we not have that”. Prepared beats frozen every time it comes up.

Let a goal she chose do the work

Something the child wants to save toward – a field trip, a toy – turns patience into a visible, personal win.

Keep it short and weekly

Fifteen minutes, once a week, one idea. Small and consistent is what turns a lesson into a belief.

Mari did not find more money or lecture her daughter. She swapped “we cannot” for “we choose,” set out three jars, and kept the right words ready – and eleven weeks later Camila was paying for her own field trip. That shift is open to any parent facing the questions that used to make them freeze.

That is the whole idea: a tight budget is not a reason to skip money lessons – it is the best classroom for them. Change “we cannot” to “we choose,” add the jars, and a child starts believing they have a say.

Learn how to teach a child about money – the same weekly plan Mari used to turn “we never can” into a nine-year-old who paid for her own field trip.

*Individual results may vary.

How do I teach a child about money on a tight budget?

What age should I start?

What do I say when my kid asks why we cannot afford something?

What is the SAVE / SPEND / SHARE jar system?

Does it work if my kids are very different?

How much time does it take?

Recommended for You