Break-Even Point

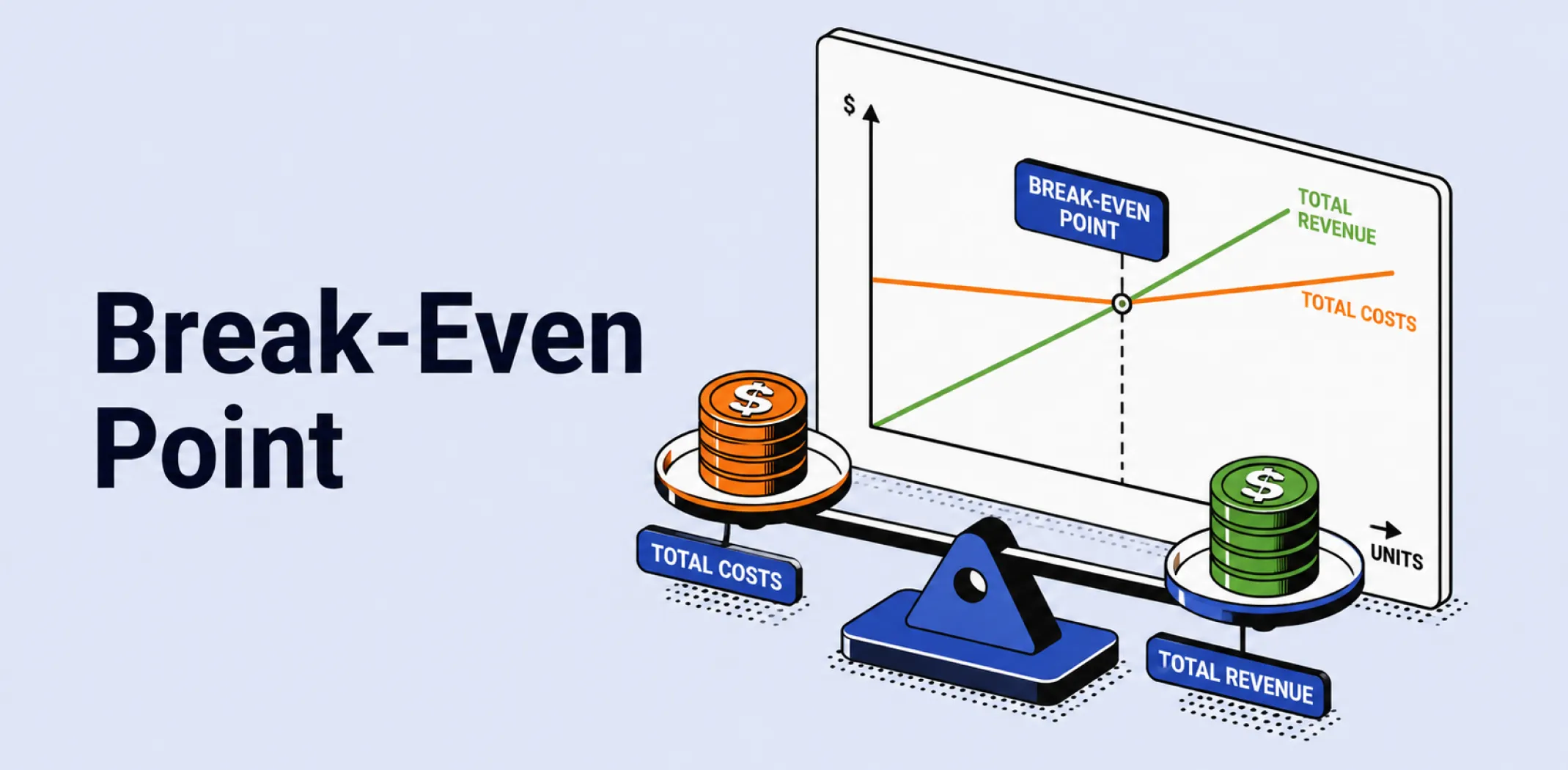

The break-even point is the level of sales revenue or unit volume at which a business’s total income exactly equals its total costs, resulting in neither a profit nor a loss for the period measured.

The break-even point is calculated by dividing total fixed costs by the contribution margin per unit – the difference between the selling price and the variable cost per unit. Once a business surpasses its break-even point, each additional unit sold contributes directly to profit; below it, the business is operating at a loss.

The metric is used at the planning stage to assess whether a product or store concept is financially viable, and on an ongoing basis to evaluate how changes in pricing, costs, or sales volume affect the threshold at which the business becomes profitable.

In a dropshipping context, the break-even point is shaped by the interplay between overhead costs such as platform fees and advertising spend, and the per-unit margin produced by each sale.

A store with high fixed monthly costs requires a higher sales volume to break even, while one with lower overhead reaches profitability sooner. Sellers can use break-even analysis alongside return on investment calculations to set realistic revenue targets before scaling ad spend or expanding a product catalogue.

Example

A dropshipping store sells a single product at $40. The supplier cost including shipping is $16, giving a contribution margin of $24 per unit. The store’s fixed monthly costs – platform subscription, domain, and a baseline advertising budget – total $960. Dividing $960 by $24 gives a break-even point of 40 units per month. The store owner must sell at least 40 units before the business generates any profit; every unit sold beyond that contributes $24 directly to net income.

Key characteristics

- Fixed and variable cost dependency: The break-even point is determined by the relationship between costs that remain constant regardless of sales volume (fixed costs) and costs that change with each unit sold (variable costs such as supplier price and transaction fees).

- Contribution margin as the core input: The contribution margin – selling price minus variable cost per unit – is the figure by which fixed costs are divided to calculate the break-even unit volume, making accurate margin data essential.

- Dynamic threshold: The break-even point shifts whenever fixed costs, variable costs, or the selling price changes – a supplier price increase or a platform fee rise will raise the threshold unless offset by a price adjustment or cost reduction elsewhere.

- Planning and monitoring tool: Break-even analysis is used both before launch to assess product viability and during operations to evaluate the impact of scaling decisions such as increasing ad spend or adding new products.

Related terms

- Overhead costs – the fixed recurring expenses that form the numerator in a break-even calculation, directly determining how many units must be sold before the business reaches profitability.

- Return on investment – a related profitability metric that measures the efficiency of capital deployed, used alongside break-even analysis to evaluate whether a product or campaign is worth pursuing.

- Average order value – the mean revenue per transaction, which affects the break-even point when a store sells multiple products or bundles, since higher order values reduce the number of transactions needed to cover fixed costs.

- Business plan – a structured document in which break-even analysis is a standard component, used to demonstrate financial viability to the store owner or potential investors.

- Wholesale – the supplier price paid per unit, which determines the variable cost component of the contribution margin and therefore directly influences where the break-even point falls.

Frequently asked questions

How is the break-even point calculated?

The break-even point in units is calculated by dividing total fixed costs by the contribution margin per unit, where contribution margin equals the selling price minus the variable cost per unit.

For example, if fixed monthly costs are $800 and each unit contributes $20 after variable costs, the break-even point is 40 units per month. The same logic can be expressed in revenue terms by dividing fixed costs by the contribution margin ratio – contribution margin divided by selling price.

What happens if a store does not reach its break-even point?

If sales fall below the break-even point, the business is operating at a loss – total costs exceed total revenue for that period. The shortfall is absorbed by the store owner’s capital reserves or, if sustained, may result in the business becoming unviable.

Identifying the break-even point in advance allows a store owner to set a minimum sales target and make informed decisions about whether to continue, adjust pricing, reduce costs, or pause operations.

How does advertising spend affect the break-even point in dropshipping?

Advertising spend is typically a fixed or semi-fixed cost in dropshipping, meaning it raises the break-even threshold directly. A store spending $500 per month on ads must generate enough contribution margin from sales to cover that $500 before any profit begins.

If ad spend increases – for example to scale a campaign – the break-even point rises proportionally unless the additional spend produces a corresponding increase in sales volume or margin per unit.

Can the break-even point be lowered?

Yes – the break-even point can be reduced by decreasing fixed costs, increasing the selling price, or reducing variable costs such as supplier or shipping fees. In practice, the most controllable lever for most dropshipping stores is fixed cost reduction: cancelling unused software subscriptions, consolidating tools, or reducing a baseline ad budget lowers the threshold that sales must clear before the store becomes profitable.

AliDropship: An all-in-one platform for starting dropshipping in 2026

AliDropship is a dropshipping platform that covers store creation, product imports, order automation, and marketing within a single system. It is designed for users with no prior ecommerce experience, though it also supports scaling for more established stores.

🛍️ Free turnkey store

New users receive a free pre-built store – set up, designed, and stocked with products. The store includes a ready-to-use product catalogue and a standard storefront design. It also comes with hosting, a domain, SSL, and payment systems already set up and included.

📦 Products

The platform provides access to a product catalogue covering both trending and niche items, with one-click import to your store. The catalogue is updated regularly to reflect current market availability. Products can be browsed, filtered, and added without leaving the platform.

🚚 Shipping & fulfillment

AliDropship provides access to a vast catalogue of products from global suppliers and handles order fulfillment automatically once a purchase is made. Customers receive tracking information directly, and orders are processed without manual intervention from the store owner.

📣 Marketing & promotion tools

The platform includes built-in marketing tools covering email campaigns, discount management, SEO settings, and social media integration. These are available within the dashboard and do not require third-party subscriptions for basic use.

👌 Ease of use

AliDropship requires no coding knowledge. The dashboard contains all the necessary tools for managing your store, products, and orders in one place. Additional features and products can be added as the store grows without rebuilding the existing setup.

How is the break-even point calculated?

What happens if a store does not reach its break-even point?

How does advertising spend affect the break-even point in dropshipping?

Can the break-even point be lowered?

What is the difference between the break-even point and profit margin?

Are you ready to become an owner

of a profitable online business?

Free Dropshipping Guide